2022 Annual Market Review

DISAPPOINTING YEAR FOR STOCKS AND BONDS

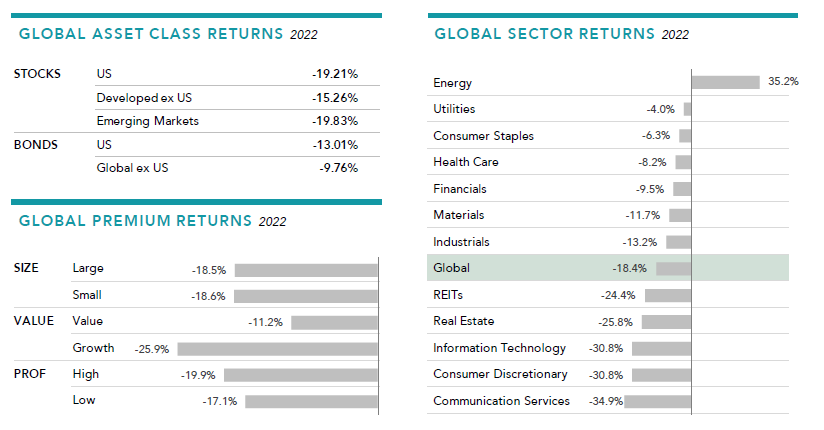

Global stocks suffered losses for the year, with the MSCI All Country World IMI Index falling by 18% following a multi-year bull market. No region was immune from the pain, with international stocks down 15% followed by U.S. and emerging market stocks down 19% and 20% respectively.

Investors were gripped with recession fears, rising oil prices, a stronger U.S. dollar, and the effects of the conflict in Ukraine. Meanwhile central banks around the globe continued their efforts to combat inflation by aggressively raising interest rates. The Fed increased rates in the U.S. seven times to over 4%, the highest level in 15 years.

ECONOMY

The coronavirus pandemic eased but remained a global concern, as did the supply chain issues that accompanied its arrival. Inflation reached a 40-year high in the U.S. and the Federal Reserve pursued a series of interest rate increases to combat rising prices, actions similar to those taken by other nations’ central banks. Russia’s invasion of Ukraine in February brought uncertainty about political stability and energy prices, among other worries. A midterm U.S. election shifted more power to Republicans but left Democrats in a stronger position than some had expected. Against this backdrop, equity and bond markets fell sharply for the year, despite several rallies.

Inflation was front and center all year long. The U.S. experienced the highest price increases in four decades, and the Fed lifted rates in a bid to reduce inflation from above 9% to the long-term target of 2%. Price increases showed signs of peaking late in the year, with inflation easing to 6.5% in the U.S. in December, although a slow retreat from multi-decade highs could keep it a concern for central banks well into 2023. Supply chain issues related to the pandemic and to Russia’s war in Ukraine also eased, and food and fuel costs declined.

The midterm elections in the U.S. left a split Congress, with Democrats narrowly controlling the Senate and Republicans taking back the House, which could affect the legislative agenda and items like tax increases and spending packages. We believe it wise to avoid focusing much on the outcome of elections, as markets have tended to reward those who stayed invested regardless of the outcome. Elections are just one of many factors influencing returns.

EQUITY MARKETS

It was an up-and-down year for markets—in the end, one with much more down than up. The S&P 500 Index fell to a two-year low in September; at one point, the index had given back 50% of its post-pandemic rally. The S&P 500 fell 18.1% for the year, its worst annual return since the financial crisis in 2008. Likewise, global stock markets ended with their largest declines since the financial crisis. Global equities, as measured by the MSCI All Country World Index, fell 18.4%. Developed international stocks, as represented by the MSCI World ex USA Index, lost 14.3%, while emerging markets declined even further, with the MSCI Emerging Markets Index down 20.1%.

While markets were down as a whole, value stocks were a bright spot for investors. Value shares have prices that are low relative to a measure like a company’s book value, and these stocks outperformed pricier growth stocks by the largest margin since 2000, at the end of the initial dot-com craze. Small capitalization stocks held their own with large cap stocks.

A RESET FOR CRYPTO AND FAANG STOCKS

If the market decline of 2022 taught investors anything, it’s that what goes up, eventually comes down. Some of the most hyped investments of the past two years did just that. Cryptocurrencies and FAANG stocks were all hit hard, with bitcoin falling below $17,000, about 75% lower than its high of nearly $68,000 in November 2021. As investors have learned by now, cryptocurrencies can be extremely volatile. From a distance, bitcoin appeared to enjoy a steady climb through much of its existence. However, there were major slumps: On three occasions since 2017, bitcoin has fallen by more than 50%, including the decline that extended into 2022.

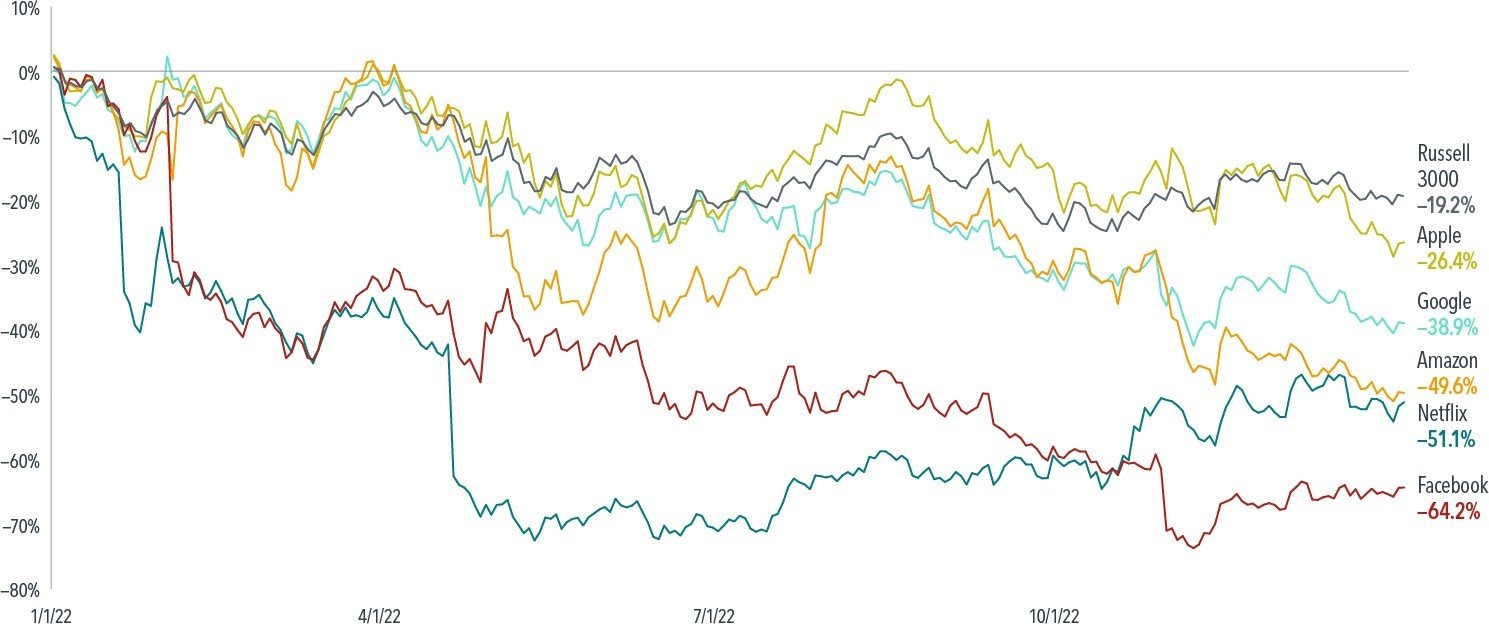

The FAANGs also saw notable declines in 2022 (see Exhibit 2). The group of tech stocks lost a combined $3.2 trillion in market value. You could say the market was de-FAANGed. Facebook parent Meta Platforms, Amazon, Apple, Netflix, and Google parent Alphabet all lagged the broad U.S. market, with Facebook and Netflix suffering particularly sharp losses. The slump came on the heels of a stellar decade— the FAANGs returned 28% per year from 2012 to 2021.

Exhibit 2

Tech Giants De- FAANGed

That reversal is a reminder that investors should be cautious about assuming past returns will continue. Even if a company with a track record of strong stock returns remains broadly successful, that may not translate to spectacular future returns. This point is borne out by looking back at stocks as they grew to become among the top 10 largest by market cap. On average, the performance of these stocks lagged the performance of the broader market within a few years of entering the top 10.

FIXED INCOME

Fixed income has typically been a safe-haven for investors, expecting bonds to rise in value when stocks fall. However, this was not the case in 2022. This tandem decline for equities and fixed income was relatively rare. Benchmark U.S. Treasuries posted their worst annual returns in decades, with 10-year Treasury notes losing 16.3%, a second straight annual loss. The last time investors saw back-to-back losses was in the late 1950s.

Higher interest rates can bring short-term pain as bond prices fall, but they can be beneficial in the long term and present new opportunities for fixed income investors. Rising yields affect fixed income portfolios in several ways. Longer-duration portfolios may experience larger immediate declines in value relative to shorter-duration portfolios as yields increase. But higher yields may lead to higher expected returns. Similarly, investors who have seen equity prices fall may be tempted to sell. But lower stock prices can be indicative of higher expected returns.

TAKING A BALANCED VIEW OF THE 60/40 PORTFOLIO

With both fixed income and equities declining on the year, the traditional 60% stock/40% bond portfolio had a hard time offering much support in either asset category, leading some to question the utility of this approach. Although 2022 was the worst year in history for many bond indices, the performance of the 60/40 portfolio didn’t crack the top five peak-to-trough drawdowns in close to a century’s worth of data. The drawdown that reached 19% at its nadir was painful, but it’s only two-thirds of the 30% peak-to-trough drawdown investors endured through a particularly difficult period from 2007–2009. And the portfolio saw some recovery late in the year, ending down 14% for 2022.

During rocky markets, it is especially important for investors to focus not solely on where returns have been but also on where they could be going. Looking at the performance of a 60/40 portfolio following a decline of 10% or more since 1926, returns on average have been strong in the subsequent one-, three-, and five-year periods (see Exhibit 3).

Exhibit 3

A Case for Optimism Performance of a 60/40 portfolio (60% S&P 500

Index/40% 5-year US Treasury notes) following a decline of 10% or more: January 1926—December 2022

LOOKING FORWARD

It can be hard to imagine an upturn when prices have fallen or when there is consternation about the direction of the economy. But history argues for persistence and patience. With the yield curve inverted, some economists are saying a recession is inevitable, if one hasn’t already begun. But history shows that across the two years that follow a recession’s onset, equities have a track record of positive performance, on average. This is an important lesson on the forward-looking nature of markets, highlighting how current prices reflect market participants’ collective expectations for the future. Likewise, U.S. equity returns following sharp declines have, on average, been positive over one-year, three-year, and five-year periods.

A look back at recent history makes a case for sticking with a plan. Strong market rebounds after steep declines can help put investors in position to capture the long-term benefits the markets offer.

Those who sold their stockholdings during the dot-com crash in the early 2000s wouldn’t have been in position to enjoy the equity recovery that eventually followed. Similarly, those abandoning a plan early in the 2008–09 financial crisis, or in March of 2020 as COVID fears spread, wouldn’t have benefited from the subsequent rallies.

As we look at prices that in some cases are well off their highs, it’s helpful to keep history in mind entering 2023. That’s the definition of thinking of investing for the long term.

Remember, we’re here to help. This also is where the time invested upfront with each of you shows its value. Formulating a solid and adaptable financial plan together and discussing liquidity, cash flows, and reserves, provides the solid footing needed for times like these with many changing facets.

We appreciate the opportunity to work with each of you. We recognize that each client’s situation is unique and incorporates different factors into their investment and financial plan.

As always, if you have any questions or concerns about current market trends and the impact on your personal situation and plan, please contact us and we would be happy to discuss.

Please follow this link to read the complete 2022 Annual Market Review.