The Quarter in Review | 3Q 2021

TOPLINE TAKEAWAYS FOR THIRD QUARTER, 2021

The third quarter of 2021 was characterized by highly volatile equity markets that closed largely unchanged. Investors struggled to reconcile continued GDP growth offset by rising inflation, supply chain bottlenecks, and tight labor markets. Overall, U.S. GDP has comfortably surpassed its pre-Covid levels. The recent softening in growth has been mainly due to a fall in consumer spending on goods. Initial concerns about the Delta variant also contributed to the slowdown.

THIRD QUARTER RETURNS

Equity markets around the globe declined for the quarter. U.S. markets were slightly down -0.10 percent for the quarter, outperforming International Developed and Emerging Markets, down -0.66 and -8.09 percent respectively. Slowing growth led to larger sell-offs in Brazil and China, off -19.95 and -17.99 for the period.

A globally diversified portfolio of 50/50 equities and fixed income declined -0.44 percent for the quarter.

FIXED INCOME

Interest rates in the U.S. increased modestly during the third quarter. Despite some intra-period volatility in bond yields, overall market levels ended the quarter roughly where they began. The Bloomberg U.S. Aggregate Bond Index returned a mere +0.05 percent for the quarter.

The Federal Reserve’s recent messaging on tapering and interest rate hikes reflects a positive overall U.S. economic picture. The Federal Open Market Committee (FOMC) has said that there is progress towards its goal of steady inflation above 2 percent and full employment. The Federal Reserve has communicated that it plans to begin reducing its quantitative easing stimulus program later this month and complete the process by the middle of 2022.

ALTERNATIVE INVESTMENTS

Commodity prices rallied for the sixth straight quarter. The Bloomberg Commodity Index was up +6.59 percent for the period and +29.13 percent for the year, topping all asset classes. Energy prices soared, led by Natural gas +58.63 percent. Agriculture and silver prices were the worst performers, down -13.89 and -16.01 percent respectively.

After surging in the first half of 2021, Real Estate Investment Trusts (REITs) were relatively flat for the quarter up a modest +1.25 percent.

THE SHIFT FROM WORKER SHORTAGE TO EMPLOYMENT DEMAND

Eighteen months ago, the concern was how are we going to get through the pandemic as tens of millions of workers suddenly found themselves unemployed. How quickly things change as the labor market is surging amid strong demand for workers, everywhere you turn companies are hiring. The question now is can businesses find enough workers to keep up with demand? This leads to the question – where have all the workers gone?

JPMorgan’s recent analysis of the situation highlighted the following for why 7.5 million works are “missing” from the pre-COVID workforce:

UI Benefits > Prior Salaries. The impact of COVID unemployment (UI) benefits on labor force participation is still unclear. It is estimated that 2.7 million people were still receiving UI benefits as of September 1 that exceeded their prior salaries, providing no incentive to return to work. With these additional benefits recently ending, there is hope these workers will begin to re-enter the workforce over the next few months.

Increased Retirements. During the pandemic, 1.5 million more people retired than usual compared to what was a steady linear trend beforehand.

Collapse in Visas granted to immigrants and non-immigrant temporary workers. While visas are starting to recover, the pandemic decline resulted in 700,000 people missing from the labor supply.

Increase in self-employment. While such individuals are still in the labor force, self-employment spiked by 800,000 once the pandemic hit.

Everyone else. Another 1.7 million people left the labor force during the pandemic for reasons other than those stated above such as COVID concerns and child-care constraints.

According to the Bureau of Labor Statistics (BLS) surveys, approximately 2 million people out of the 7.5 million missing workers intend to search for work again at some point, and we do expect an increased labor supply as we move into 2022.

Lastly, out of necessity, businesses have begun adapting to having fewer available workers through an increased focus on automation.

HOUSEHOLDS REALIZING RECORD AMOUNTS OF CASH

The excess cash provided through a combination of various federal programs (one-time checks, PPP loans, extended unemployment, student loan waivers, moratorium on evictions, etc.) has provided ample liquidity for consumers to continue to drive demand for some time. If you look at the figures below it is quite staggering to say the least. Pre-Covid, there was a total of $13.6 Trillion in US Household Bank Accounts. As of last summer, just 15 months after the start of the pandemic, that figure jumped to $17.4 Trillion, an increase of $3.8 Trillion – during a pandemic, nonetheless.

INFLATION – HERE TO STAY OR JUST TRANSITORY?

This is another question that is being asked by consumers and investors alike. Inflation typically arises when demand outpaces supply. When ample dollars chase too few of something (goods, workers, services) prices tend to go up. So where are we today?

Ample cash – households are flush with cash (see above, $3.8 Trillion more than a year ago)

Tight Labor Market

Unemployment is at 4.8% nationally, 2.8% for those with a college degree

JOLTS (Job Openings and Labor Turnover Survey) registered over 10 million open positions

Strong Economic Growth – GDP has been growing at > 5 percent the last several quarters

Manufacturing output (and corresponding distribution) has taken months to restart post-Covid and is not keeping up with current demand.

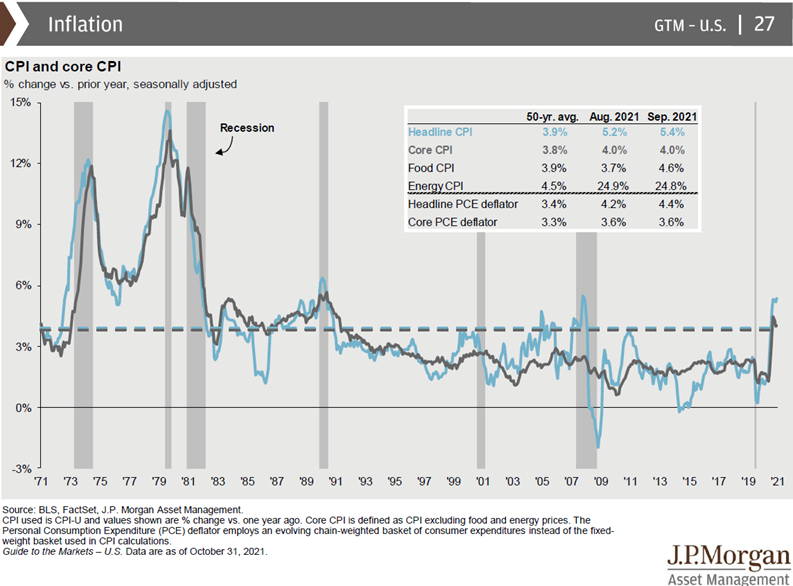

As outlined in the chart below, September Core CPI (excludes food and energy) stood at 4.6 percent after hovering around 2 percent for the last several decades. Given the data above, this should not be a surprise. Separately, Energy and Food CPI registered at 24.8 and 4.6 percent respectively.

We would anticipate goods-related inflation to continue on for a number of quarters as supply chain issues continue to be worked through, hopefully with progress being made in the first half of 2022.

However, in regard to higher labor rates as we highlighted last quarter, we see those being here to stay for some time. Once you start paying employees higher wages (current and new hires), you typically do not see those being taken back down just because demand has normalized. As a result, wage pressures and labor shortages may be an endemic feature of the post-COVID U.S. economy continuing to drive inflation higher and for a longer period of time.

SUMMARY

Every quarter and every year there are always going to be items that give you pause and concern; but there also are things to feel positive about, and here are just a few occurring right now:

U.S. Manufacturing came in with the 17th straight month of growth, solidly in expansion

ADP Jobs report noted that the economy added 571,000 jobs in October

Consumer confidence continues to tick upwards

With 2/3 of the S&P500 companies having reported their third quarter results, overall revenue is up 19 percent and earnings are up almost 40 percent from the same period a year ago.

The economy still experienced solid growth – even with all of the supply chain bottlenecks

As we reflect back to where we were more than a year ago, things were much different and volatile. Having core principles to fall and lean into were – and remain – critical to managing through the challenges. For us, this involves:

Having an Investment PLAN

Aligning your portfolio from both a RISK and GOALS perspective

Understading HOW you are invested and WHY

Staying DISCIPLINED and PATIENT

Remember, we’re here to help. This also is where the time invested upfront with each of you shows its value. We recognize that each client’s situation is unique and incorporates different factors into their investment and financial plan. Formulating a solid and adaptable financial plan together and discussing liquidity, cash flows, and reserves, provides the solid footing needed for times like these with many changing facets.

We are grateful for the opportunity to work with each of you. As always, if you have any questions or concerns about current market trends and the impact on your personal situation and plan, please contact us and we would be happy to discuss.

We wish you, your families, friends, and colleagues all the best as we rapidly move towards year end and the holiday season.

Please follow this link to read the complete Quarterly Market Review | 3Q 2021.