The Quarter in Review | 3Q 2022

GLOBAL SLOWDOWN CONTINUES

The global economy continued to slow amid the backdrop of 40-year high inflation, tight labor markets, and continued aggressive tightening by the Federal Reserve. Financial conditions continued to tighten in the form of higher borrowing costs, which is beginning to slow demand, most notably in the housing market.

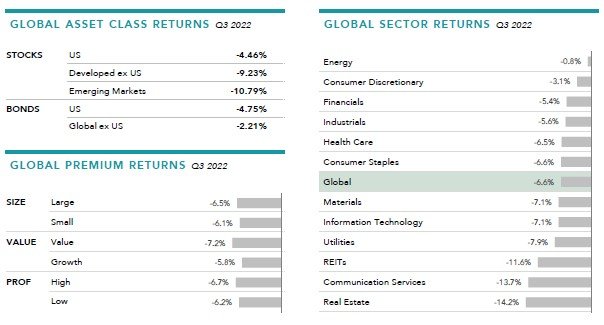

U.S. stocks bounced off their June 16 lows but still finished the quarter down -4.46 percent. Internationally Developed and Emerging Market stocks fared worse, down -9.20 and -11.5 percent respectively.

On a year-to-date basis through the end of the third quarter, U.S. stocks were down -23.9, Internationally Developed -26.8 and Emerging Markets -27.9 percent respectively.

Small and large cap stocks have performed about the same. However, on a relative basis, Large Cap U.S. Value based stocks have significantly outperformed all other equity classes.

FIXED INCOME

The Fed continued to aggressively tighten monetary policy in the third quarter and signaled it will continue to do so to combat high inflation. Short-term Treasury yields are now higher than longer term yields resulting in an inverted yield curve.

As interest rates continue to march up, the Bloomberg U.S. Aggregate Bond Index continues to slide down, declining -4.75 percent for the quarter and is now down -14.61 for the year.

ALTERNATIVE INVESTMENTS

Given the increasing global recession concerns and the continued strengthening of the U.S. Dollar, the Bloomberg Commodity Index extended declines from the second quarter into the third quarter, down -4.11 percent for the period. Crude Oil and Unleaded Gas were the worst performers, returning -21.51% and -20.53% during the quarter, whereas Natural Gas and Corn were the best performers over the same period returning +24.49% and +8.01%.

Due to the continued rise in interest rates, Real Estate Investment Trusts (REITs) continued to decline and is the worst performing asset class to date in 2022, down -10.37 percent for the quarter and -29.32 year-to-date.

ECONOMY

After a strong rebound from the pandemic in 2021, it has been all downhill for the global economy this year. Economic activity is being hindered as the Federal Reserve deals with the hottest inflation in decades, impairments from the Ukraine war, and China’s prolonged COVID lockdowns disrupting supply chains.

Last week’s Consumer Price Index (CPI) report showed a 7.8 percent year-over-year increase, down from a 9 percent reading in June. A number of commodity prices (oil, steel, copper, cotton, sugar and aluminum) have been trending down for several months. These declines have been offset by higher wages and rents. We might have reached peak inflation, but it will take some time for inflation to move back down as monetary policies have a lag. Based on how the CPI is calculated, mathematically it is almost impossible for the CPI to drop into the Fed’s targeted range until at least Summer of 2023.

We know that each cycle is different and this one has its own characteristics. We are in unchartered territory with the unique combination of high inflation, tight labor market (3.7 percent unemployment), rapidly escalating interest rates combined with declining corporate earnings. Through its inaction in 2021, the Fed greatly damaged its credibility by allowing inflation to reach far above its target. If it were to prematurely abandon its commitment now, it would be a double blow to its integrity and difficult to restore.

The Fed has been telling us it has the tools at its disposal to adequately quell inflation without moving us into a recession. Its track record indicates a potentially different outcome.

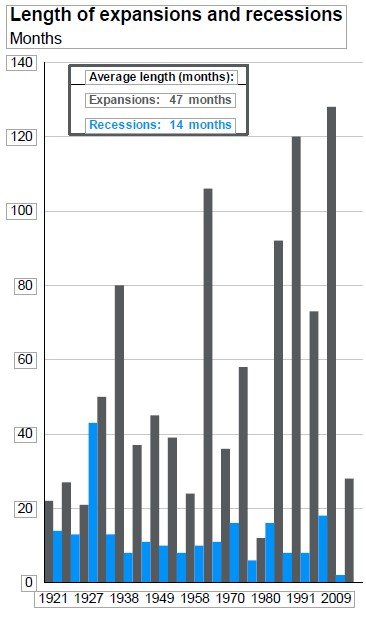

The word “recession” is defined as generalized economic pain. Business activity slows, people lose jobs and income, and asset values fall. Not all feel the same degree of pain, but everybody feels something.

Recessions are not rare but typically do not last that long. They are part and parcel of economic cycles. As the table below shows, there have been 17 recessions in the last 100 years. The average length of a recession over this period has been 14 months, or a little over a year. As each recession is different, the question we all face as we approach the recession average is – how long and how severe will this one be?

LOOKING FORWARD

We are in a distinctive and trying environment with the rare combination of a decelerating economy and rising interest rates, the result of which leaves us with few good investment alternatives. That said, history provides needed perspective, and a thoughtful investment plan proves valuable now more than ever.

U.S. Treasuries are generally considered a “risk free” security and in high demand when the stock market struggles. However, as of this writing the 10-Year Treasury index is down nearly 17 percent. As the graph below illustrates, bond market losses have been rare and relatively small. Prior to 2022, it has been more than 40 years since the bond market has lost over 10 percent in one year.

Investors have never endured the double hit of negative returns in both equities and fixed income in the same year as they have so far in 2022. It has been 14 years since the stock market has fallen as much as it has this year (in 2008, the S&P 500 lost 37 percent). Unlike this year, Bonds returned over 20 percent in 2008 as the Fed was aggressively cutting interest rates in response to the collapse in real estate and the mortgage bond market.

To date in 2022, the Vanguard Total Bond Market Index is down 15 percent and the S&P 500 almost 20 percent. This is the first time since 1969 (well over 50 years ago) that both equities and fixed income will be on track to deliver negative annual returns in the same year.

Markets drop, Bear markets arrive. That is an unavoidable part of investing. We can neither control what the Federal Reserve does, nor predict what happens to corporate profits. What we can control is how we respond.

We have included the chart below to remind us of the typical characteristics of bear markets. Similar to recessions, although a recession doesn’t always lead to a bear market, there is pain but typically it does not last that long. During the last 60 years there have been nine Bear markets, on average they’ve lasted 14 months with an average decline of 37 percent. Looking at just the colors, what jumps out is the proliferation of Bull/Blue market years compared to the down ones.

Investing in markets has always been and continues to be uncertain. Hoping the Federal Reserve will be able to navigate a “soft landing” as it continues to tighten (raise) interest rates into an economic slowdown, we are reminded that “hope” is not a strategy nor is it an investment process.

Investing is as much about managing risks as it is managing returns. As we say often, risk happens slowly and then all at once. It is why we remain rooted and focused on a deliberate process we map out with each of you rather than reacting to market fluctuations.

HAVE AN INVESTMENT PLAN

An investment philosophy serves as a compass to guide you through turbulent times. When you have a compass, it doesn’t take drastic directional changes to find your way. Establishing and adhering to a well thought out investment plan, ideally agreed upon in advance of periods of volatility, you can remain confident and calm during periods of short-term uncertainty.

ALIGN PORTFOLIO RISK WITH GOALS

As investors, our collective appetite for risk often changes based on the market environment we are in. You want to have a plan in place that gives you peace of mind regardless of the market conditions.

STAY DISCIPLINED / BE PATIENT

Financial downturns are unpleasant for all market participants. While no one has a crystal ball, adopting a long-term perspective can help change how you view market volatility.

Remember, we’re here to help. This also is where the time invested upfront with each of you shows its value. Formulating a solid and adaptable financial plan together and discussing liquidity, cash flows, and reserves, provides the solid footing needed for times like these with many changing facets.

We appreciate the opportunity to work with each of you. We recognize that each client’s situation is unique and incorporates different factors into their investment and financial plan.

As always, if you have any questions or concerns about current market trends and the impact on your personal situation and plan, please contact us and we would be happy to discuss.

May you enjoy a wonderful Thanksgiving Day and a joyous Holiday Season.

Please follow this link to read the complete Quarterly Market Review | 3Q 2022.